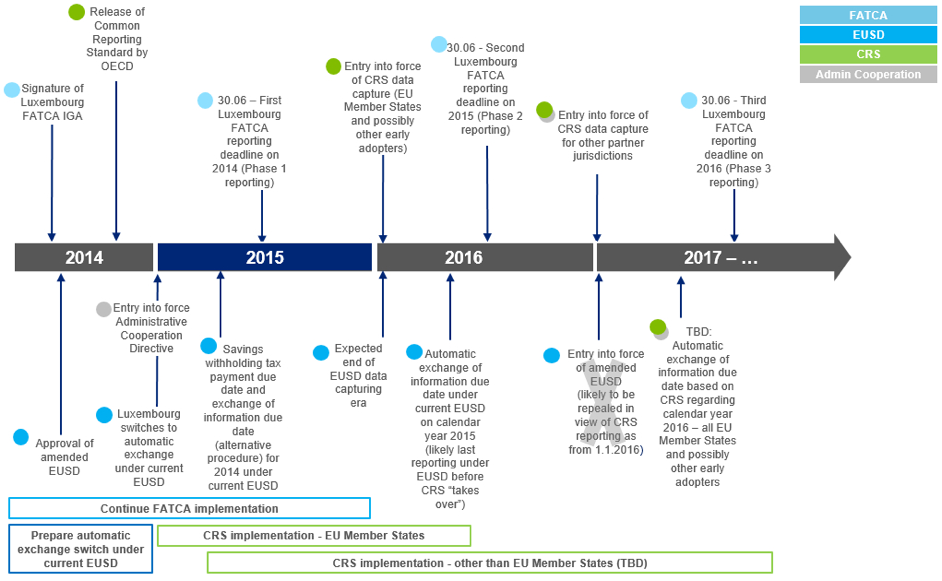

On 24 December 2015, the Luxembourg Parliament transposed in national law the Directive 2014/107/EU. The new Rules have entered into force on 1 January 2016, with the first wave of requirements, in particular the on-boarding of New Account Holders. The first reporting under CRS law was performed by the end of June 2017 on 2016 financial account information.

Much like FATCA provisions, the CRS makes FIs (Financial Institutions) review and collect information on their clients/investors, in order to identify their tax residence, as well as to provide certain account information to relevant foreign tax authorities (via the Luxembourg tax authorities) on an annual basis.

The CRS will enhance the automatic exchange of information, will establish a common standard for all participating jurisdictions and will facilitate identification of beneficial owners.

Table of Contents

New Account holders

- Luxembourg FI’s have to obtain a self-certification mentioning the name, address, tax residence, tax identification number (TIN) and place and date of birth (for individuals) of the account holder upon account opening.

- All account holders subject to CRS review have to issue a self-certification form in which they state their residence for tax purposes and provide their TIN. Without a self-certification, the FI is legally bound to consider the account holder as a reportable person and act accordingly towards the relevant tax authorities.

Due diligence regarding preexisting Accounts

- The law clarifies that Luxembourg FIs must apply their due diligence procedures to all their non-Luxembourg resident clients and investors. It allows Luxembourg FIs to apply the procedures governing new accounts to preexisting accounts.

- A Reporting Financial Institution may not rely on a self-certification or Documentary Evidence if it knows or suspects that the self-certification or Documentary Evidence is incorrect or unreliable.

Reporting

- Luxembourg FIs have to submit their first reports to the Luxembourg tax authorities no later than 30 June 2017.

- Luxembourg reporting FIs have to to file a report with the Luxembourg tax authorities even if they haven’t identified any reportable accounts.

Control and penalties

- A reporting Luxembourg FI’s omitting to comply with due diligence rules or to introduce procedures in view of reporting are liable to a penalty up to EUR 250,000.

- A reporting Luxembourg FI’s omitting to file the required report or if it files a late, incomplete or inaccurate report, it may be liable to a penalty of 0, 5% of the amounts that should have been reported, with a minimum of EUR 1,500.

Data protection rules

- Reporting Luxembourg FIs can’t invoke any professional secrecy rules to refuse the reporting of required information.

- Reporting Luxembourg FIs should inform each individual that information will be collected and possibly reported.

- Reporting Luxembourg FIs must communicate to individuals the following:

- The Luxembourg FI is responsible for personal data processing.

- The personal data is intended to be used for the purpose of the CRS.

- The data will be reported to the Luxembourg tax authorities and the tax authorities of the jurisdiction(s) of residence of the Account Holders or Controlling Persons of a Passive NFE.

- The reported individual has the right to access the data/financial information reported to the Luxembourg tax authorities and to rectify it.

- Reported individuals have to reply to each information request sent to them. The Reporting Luxembourg FI must also inform them what may happen if the fail to answer.